Auto insurance gap coverage pays the difference between a car’s actual cash value (ACV) and its outstanding loan or lease balance in case of a total loss. This lets drivers avoid paying off a loan on a car they no longer use following a total loss or theft.

Gap coverage can be particularly helpful for new cars with longer auto loans. The principle on long loans decreases slowly at first but a new car quickly loses value. After one year on a loan of six years, 86% of a loan’s balance remains. But an average car retains only 80% of its value after one year. The difference on a $20,000 car loan would be 6% of $20,000 or $1,200. That is a lot of money for an average American. Gap coverage can eliminate this risk.

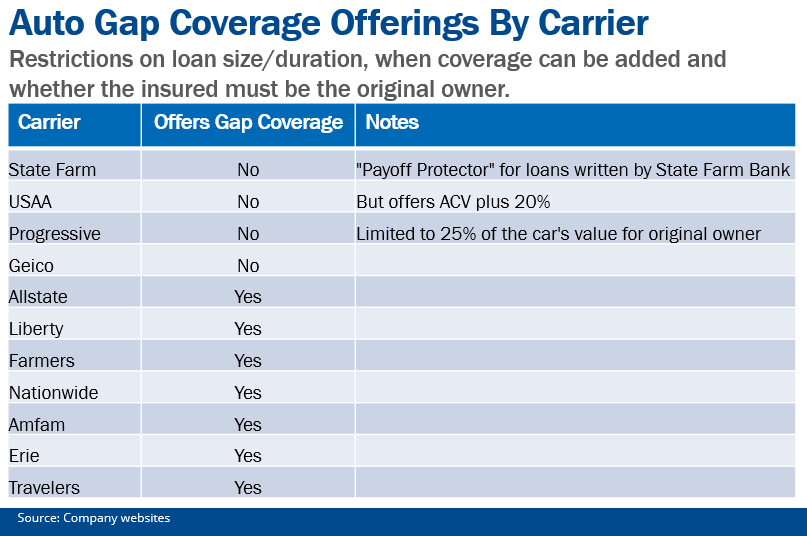

Which Carriers Offer Gap Coverage

But not all carriers offer gap coverage. State Farm, Geico, Progressive, and USAA do not offer gap coverage.

But not all carriers offer gap coverage. State Farm, Geico, Progressive, and USAA do not offer gap coverage.

- State Farm used to offer Payoff Protection on loans taken out through State Farm Bank but that stopped on new loans when US Bank took over State Farm bank.

- Geico does not offer gap coverage at all.

- USAA does not offer gap coverage but allows customers to buy coverage which pays ACV plus 20%. The extra amount can be used to pay off a loan if the ACV is not enough.

- Progressive says that it does not offer gap coverage but it does offer loan/lease payoff coverage. This is very similar to gap coverage but it is limited to 25% of the car’s actual cash value regardless of the amount of the outstanding loan/lease.

Common Restrictions

Many carriers put restrictions on their gap coverage. Typical restrictions include the size and duration of the loan, when the coverage can be added, and whether the insured must be the original owner. Many carriers require the coverage to be added when the car is first purchased by the insured. Some carriers bundle gap coverage with their new car replacement endorsement.

What To Do With This Information

Agents affiliated with carriers which offer gap coverage should mention gap coverage which is usually very affordable and can help an insured avoid a large payoff if a car is totaled or stolen in its early years.

The coverage should usually be removed once the car’s ACV exceeds the balance on a loan. Most auto loans last no longer than 6 years while a car will typically last for 12+ years. At some point, the car’s ACV will exceed the loan so the coverage should be removed. Agents will want to check their book for customers with gap coverage to see if they still need it. Removing unnecessary coverages can build trust and support cross sales.

Importantly, buying gap coverage through an insurance agent is usually less expensive than buying it through an auto dealer.

Agents with carriers which do not offer gap coverage can point out that the coverage is offered from auto dealers and gap coverage is usually only valuable for a few years.