Conning & Co, one of the most watched experts in the insurance industry released its forecast for the rest of 2026 and they expect slowing premium growth in both auto and homeowners’ lines.

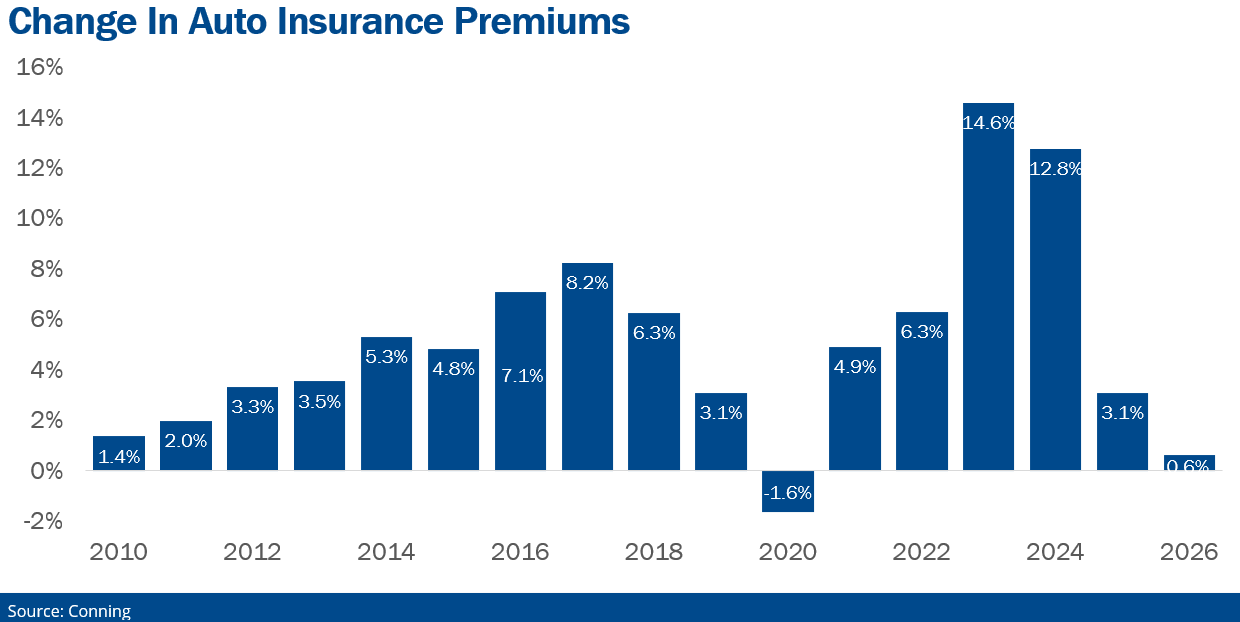

Auto Insurance Forecast: 0.6% Growth In 2026

On the auto side, Conning forecasts premiums to grow in 2026 by just 0.6%, the lowest growth rate since 2009 excluding the pandemic year of 2020. When 2026 began, Conning forecast growth of a larger but still low 2.3%.

On the auto side, Conning forecasts premiums to grow in 2026 by just 0.6%, the lowest growth rate since 2009 excluding the pandemic year of 2020. When 2026 began, Conning forecast growth of a larger but still low 2.3%.

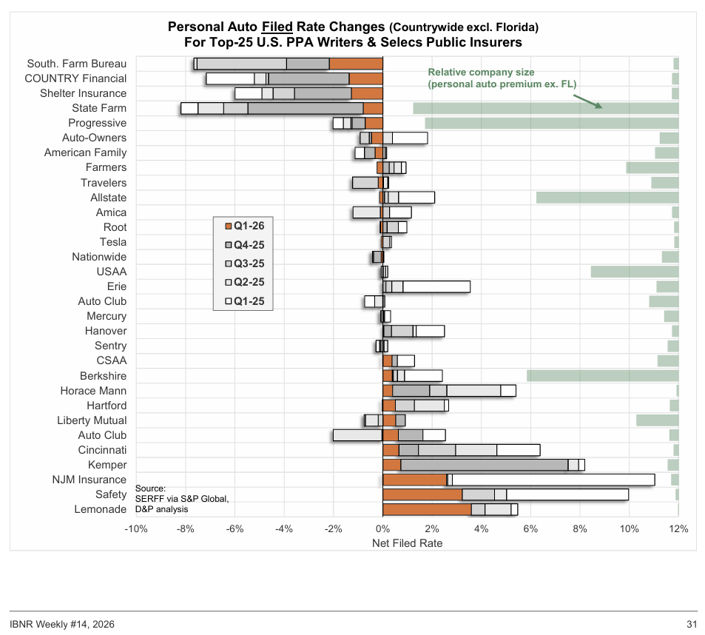

What happened? The Progressive-State Farm competition to be the nation’s largest auto insurer led to significant rate reductions in 2025 and that forced the rest of the industry to follow suit in 2026. Dowling & Co report that Southern Farm Bureau, Country Financial, and Shelter led all top 25 carriers with the largest rate decreases in 2026. See the attached chart. The decreases of these three carriers were larger than State Farm’s decreases although State Farm’s cuts ranked fourth in the top 25 and number one in the top 10.

What happened? The Progressive-State Farm competition to be the nation’s largest auto insurer led to significant rate reductions in 2025 and that forced the rest of the industry to follow suit in 2026. Dowling & Co report that Southern Farm Bureau, Country Financial, and Shelter led all top 25 carriers with the largest rate decreases in 2026. See the attached chart. The decreases of these three carriers were larger than State Farm’s decreases although State Farm’s cuts ranked fourth in the top 25 and number one in the top 10.

We reported earlier that there is unlikely to be another round of rate cuts after the current round. State Farm already cut rates below the level supported by its actuaries and its $5 billion dividend will improve retention without needing to cut rates more.

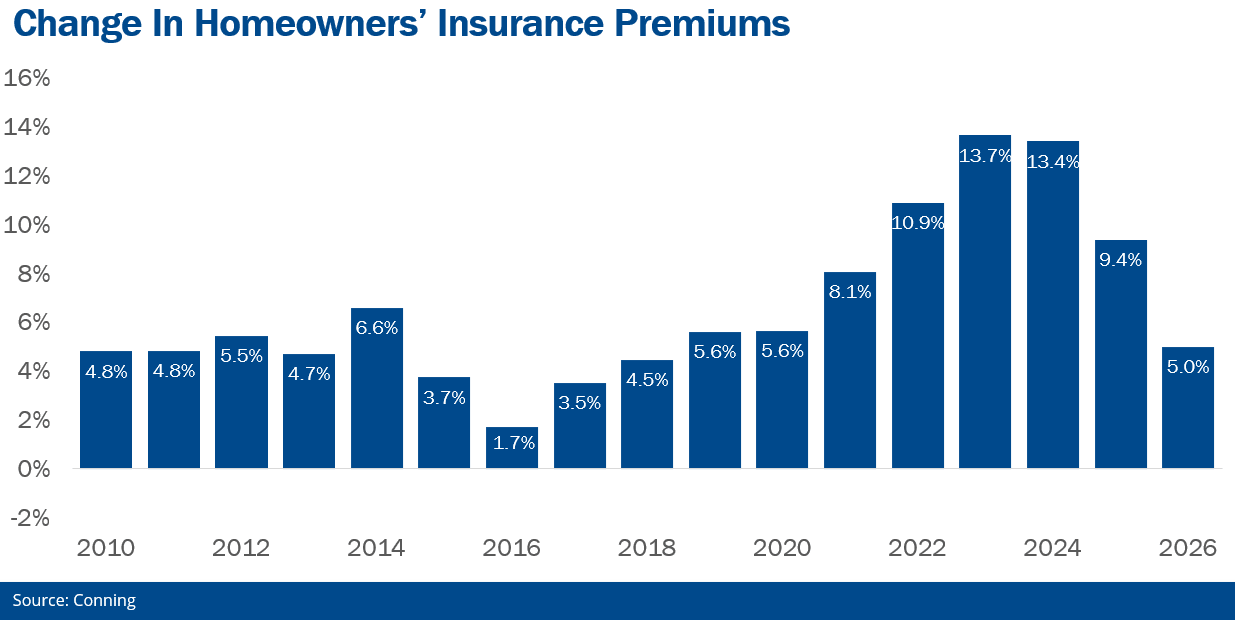

Homeowners’ Insurance: 5.0% Growth In 2026

Conning cut its forecast homeowners’ premium growth for 2026 from 8.4% in Q4 2025 to 7.4% at the beginning of 2026 to 5.0% today. The declining growth is largely due to lower catastrophes in the second half of 2026, “shrinkflation”, and the declining cost of reinsurance.

Conning cut its forecast homeowners’ premium growth for 2026 from 8.4% in Q4 2025 to 7.4% at the beginning of 2026 to 5.0% today. The declining growth is largely due to lower catastrophes in the second half of 2026, “shrinkflation”, and the declining cost of reinsurance.

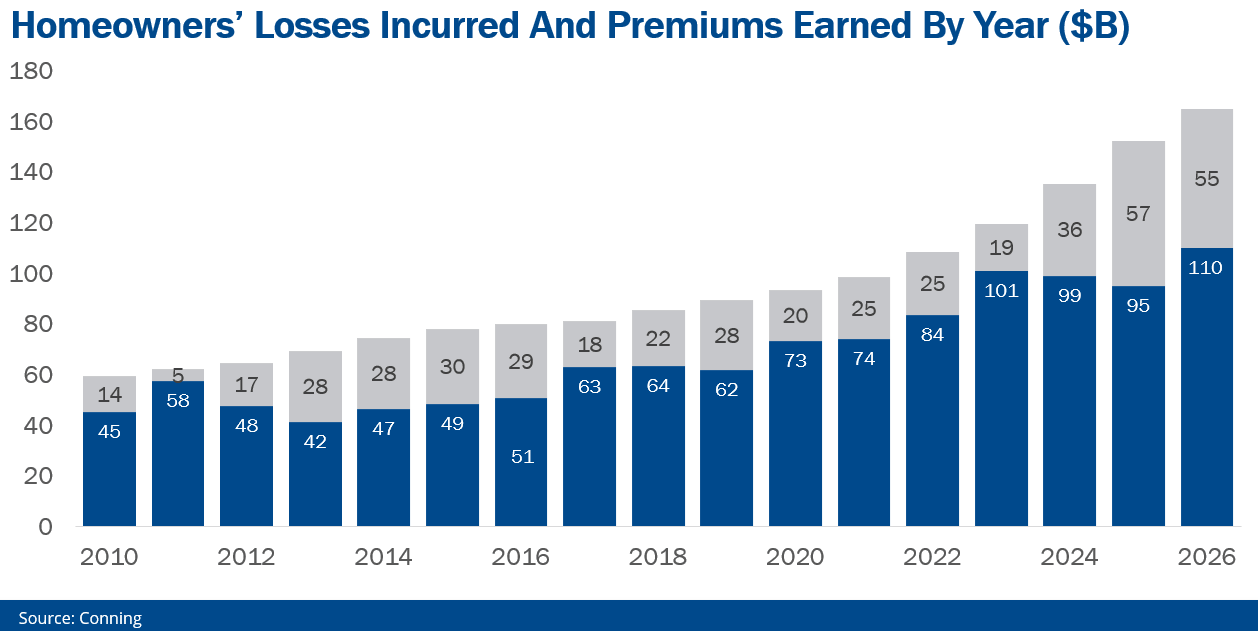

In 2025, the homeowners’ insurance industry enjoyed its lowest loss ratio in a decade thanks to rising premiums and slightly lower claims costs. It is important to note that if homeowners’ claims for the rest of 2026 meet expectations, the industry will incur higher dollar losses in 2026 than in any previous year, $110 billion. But the industry has already increased rates enough to cover this cost. Insurers believe they have a handle on Mother Nature’s “new normal” level of wind and hailstorms. Rate hikes will still happen, particularly in wildfire areas, but the level of increase will be much more moderate than in the past.

In 2025, the homeowners’ insurance industry enjoyed its lowest loss ratio in a decade thanks to rising premiums and slightly lower claims costs. It is important to note that if homeowners’ claims for the rest of 2026 meet expectations, the industry will incur higher dollar losses in 2026 than in any previous year, $110 billion. But the industry has already increased rates enough to cover this cost. Insurers believe they have a handle on Mother Nature’s “new normal” level of wind and hailstorms. Rate hikes will still happen, particularly in wildfire areas, but the level of increase will be much more moderate than in the past.

“Shrinkflation” is also keeping rates in check. Insurers are increasing deductibles and lowering coverage. Decreases in coverage come in the form of mandatory changes in policy language such as anti-matching clauses as well as voluntary endorsements that limit coverage in exchange for lower premiums. More on this trend in tomorrow’s article.

What To Do With This Information

Agents should expect a slight cooling in shopping as rate increases slow. This does not mean that shopping will be low for the rest of 2026—it will not. But it may cool a bit from the record levels it was at in 2025. Shoppers are still likely to be multiline since homeowners’ insurance rates are increasing at a much faster rate than auto insurance rates.